Have you ever calculated what it would actually cost to lose your home — not the outstanding mortgage balance, but everything else tethered to that address: the school your child attends, the neighbor who has your spare key, the street you can navigate in the dark without thinking? That is not an abstract question for Wanda Ramos. For the better part of two years, it was the only question that mattered.

I first heard about Wanda at a block party in Detroit’s Bagley neighborhood last summer. A mutual neighbor mentioned her situation quietly, the way people share stories they feel deserve more attention than they’re getting. Wanda was standing across the yard and caught my eye when she realized she was being described. She gave a small, tired nod. A few days later, she agreed to sit down with me at her kitchen table.

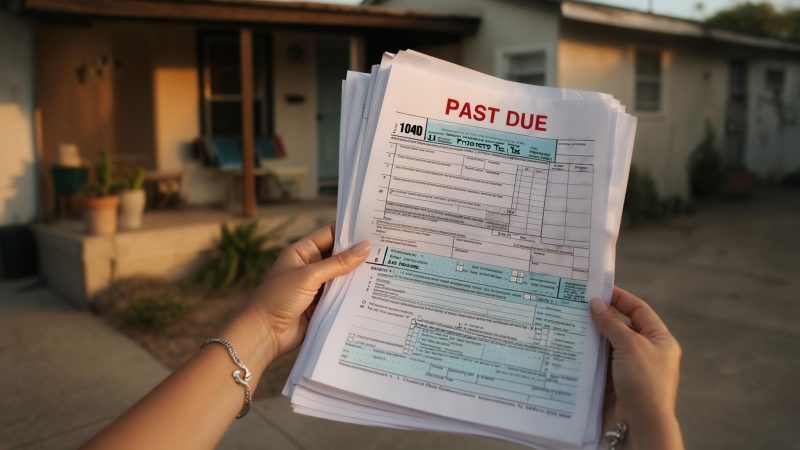

She is 39 years old, a registered nurse at a Detroit hospital, and a single mother raising a nine-year-old daughter named Maya. Her ex-partner provides no financial support. She runs a side business reselling vintage furniture she finds at estate sales on weekends. She is, by every visible measure, someone who does not stop moving. But by early 2025, she was $4,800 behind on her property taxes — and Wayne County’s foreclosure clock had started ticking.

How a Car Repair and a Childcare Hike Started a Two-Year Spiral

Wanda bought her three-bedroom bungalow in 2018 for $89,000. Her monthly mortgage payment is $987, and she has never missed one. Property taxes in Wayne County are billed separately — a detail that matters more than it sounds, because it means a homeowner can be perfectly current on their mortgage and simultaneously delinquent on taxes without any early warning from their lender.

The trouble started in fall 2022. Her car engine seized, and the repair ran $2,400. The same month, the childcare subsidy program she and Maya depended on recalculated its income thresholds, and her after-school care costs jumped by $180 a month overnight. She had no emergency fund large enough to absorb both hits.

By the end of 2023, her unpaid property tax balance had grown to approximately $2,200, compounded by Wayne County’s statutory interest charges. She received a formal delinquency notice that winter — the first time the weight of it fully landed. By January 2025, the total had reached $4,800. Under Michigan law, a property becomes eligible for tax foreclosure after three years of continuous delinquency. Wanda was approaching year three.

The Program a Coworker Mentioned — and What Wanda Found When She Looked

Wanda said she did not know that property tax assistance programs existed until a hospital colleague mentioned the Wayne County Treasurer’s Avoid Foreclosure initiative during a break room conversation in February 2025. That night, she went home and spent three hours reading everything she could find online.

What she landed on was Detroit’s Pay As You Stay program — known as PAYS — administered through a partnership between the Wayne County Treasurer’s office and several nonprofit housing organizations. PAYS is designed for owner-occupants of modest-value homes who have fallen behind on taxes. Qualified participants can have a portion of their penalty interest forgiven, then enter a structured payment plan for the reduced remaining balance.

Applying was not simple. As Wanda explained to me, she needed two years of tax returns, proof of residency, a copy of her mortgage, current pay stubs, and documentation of all household income including her furniture resale earnings. “I’m a nurse,” she said, “I’m used to paperwork. But this was a different kind of stress — because these weren’t forms about someone else’s health. They were about whether my daughter and I would still have a home.”

She submitted her complete application through United Community Housing Coalition in early March 2025. She was told processing would take six to eight weeks.

The Approval Letter She Read Four Times

Wanda’s PAYS application was approved in mid-April 2025 — six weeks after submission, landing on the shorter end of the window she’d been given. Based on her income of roughly $58,000 per year and her home’s assessed value, a portion of her penalty interest was forgiven. Her restructured obligation came to approximately $3,200, payable at $180 per month over 30 months.

She also applied — separately — for the Michigan Homestead Property Tax Credit, a state program administered through the Department of Treasury that provides a credit to lower-income homeowners whose property taxes exceed a qualifying percentage of their household income. For tax year 2024, Wanda received a credit of approximately $850, which she applied directly toward her current-year tax bill — keeping new delinquency from building while she paid down the old balance.

What the Relief Didn’t Solve — and What Keeps Wanda Up at Night

Sitting at her kitchen table with Maya’s crayon drawings taped to the refrigerator behind her, Wanda looked lighter than I expected. The immediate crisis — the accelerating foreclosure timeline — had been interrupted. But she was careful not to frame any of it as a resolution.

Her retirement savings sit at approximately $11,000 in a hospital 403(b) account. She is 39. She said the number out loud with a visible wince. “I know what nurses’ retirements look like when they don’t plan,” she told me. “I’ve watched it happen to people I respect. And I don’t want that to be me.”

Her weekend furniture resale business brings in between $400 and $700 a month depending on estate sale inventory. She is actively exploring nursing agency work — contract shifts at other hospitals — that could add another $600 to $800 monthly without requiring a second full-time commitment. “I’m always looking for the next thing,” she admitted. “It’s probably exhausting to be around. But I bought this house so Maya would have stability. If I have to hustle to keep it, that’s what I’m going to do.”

The PAYS installment of $180 per month runs through mid-2027. There is little margin. Wanda acknowledged that another unexpected expense — another car failure, another policy shift in childcare subsidies — could put pressure on the payment plan and restart the delinquency cycle. “The program saved me this time,” she said. “I just have to make sure there isn’t a next time.”

What Wanda’s Story Reveals About Housing Help for Working Homeowners

Wanda’s experience reflects a pattern that housing advocates and researchers have tracked in Detroit for years. Property tax delinquency and foreclosure have disproportionately affected working-class owner-occupants — people who are current on their mortgages but cannot absorb the full weight of a separately billed, annually compounding tax obligation after a single financial disruption. Researchers at the University of Michigan have documented that tens of thousands of Detroit homes were lost to tax foreclosure between 2010 and 2020, many belonging to long-term owner-occupants who were unaware that assistance programs existed.

Both PAYS and the Michigan Homestead Property Tax Credit are real, functional programs — but neither reaches eligible homeowners automatically. Both require an active application, documentation, and in PAYS’s case, navigation through a nonprofit intake partner. Wanda learned about her options through a coworker’s passing comment, not through any outreach from the county or state.

Before I left that afternoon, Wanda walked me to her front door and paused at a framed photo of Maya hanging in the hallway. She said the two years of delinquency had forced her to research every program she might qualify for, rather than assuming her income made her ineligible. The assumption of ineligibility, she said, had cost her time she did not have.

“Nurses don’t think of themselves as the people who need help,” she said quietly, still looking at the photo. “That’s something I had to get over.”

That line has stayed with me since. Wanda’s story does not end with financial security — the payment plan runs to mid-2027, her retirement balance is thin, and the next disruption is always closer than it seems. But she knows the landscape now, the programs, the paperwork, the phone numbers at the housing coalition. That knowledge, she told me, is its own kind of ground to stand on.

Related: She Got a Raise, Then Retired at 25 — Now She’s $5,400 Behind on Property Taxes and Underwater on Her Car

Related: A Columbus Social Worker Was $4,200 Behind on Property Taxes — What He Found After He Finally Stopped Refusing Help

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply