Most people assume that government housing programs exist only for the very poor. That assumption, it turns out, can leave middle-income homeowners completely exposed when things go wrong — and in Tommy Dawkins’s case, several things went wrong at once.

I first connected with Tommy through the Southside Community Resource Center in Birmingham, Alabama, which had referred his story to Benefit Reporter after staff there saw him navigating a housing insurance crisis largely on his own. When I sat down with him in a small conference room at the center on a Tuesday morning in late February 2026, he arrived with a manila folder thick with letters, policy notices, and handwritten notes. He was composed, even upbeat — but his eyes gave away a wariness that hadn’t fully left him.

Tommy is 66 years old, widowed, and works as a marketing manager at a Birmingham tech startup. His two adult children live out of state. He owns a three-bedroom home in the Avondale neighborhood that he and his late wife bought in 2009 for $187,000. On paper, he is not someone most people would picture sitting in a community center asking for help.

When Income on Paper Doesn’t Match Life on the Ground

Tommy’s base salary at the startup is $71,500 a year — a solid income by most measures. But for the past four years, his total take-home had been closer to $89,000 annually, padded by consistent overtime that his employer had quietly relied on as a workaround for understaffing. In March 2025, that changed. The startup restructured its marketing department and capped all overtime across the board.

“I didn’t get fired. I didn’t get a pay cut on paper,” Tommy told me, spreading his hands on the table. “But I lost about $17,500 a year overnight. That’s not nothing when you’re running a house alone and you’re six years from a retirement you’ve been planning for.”

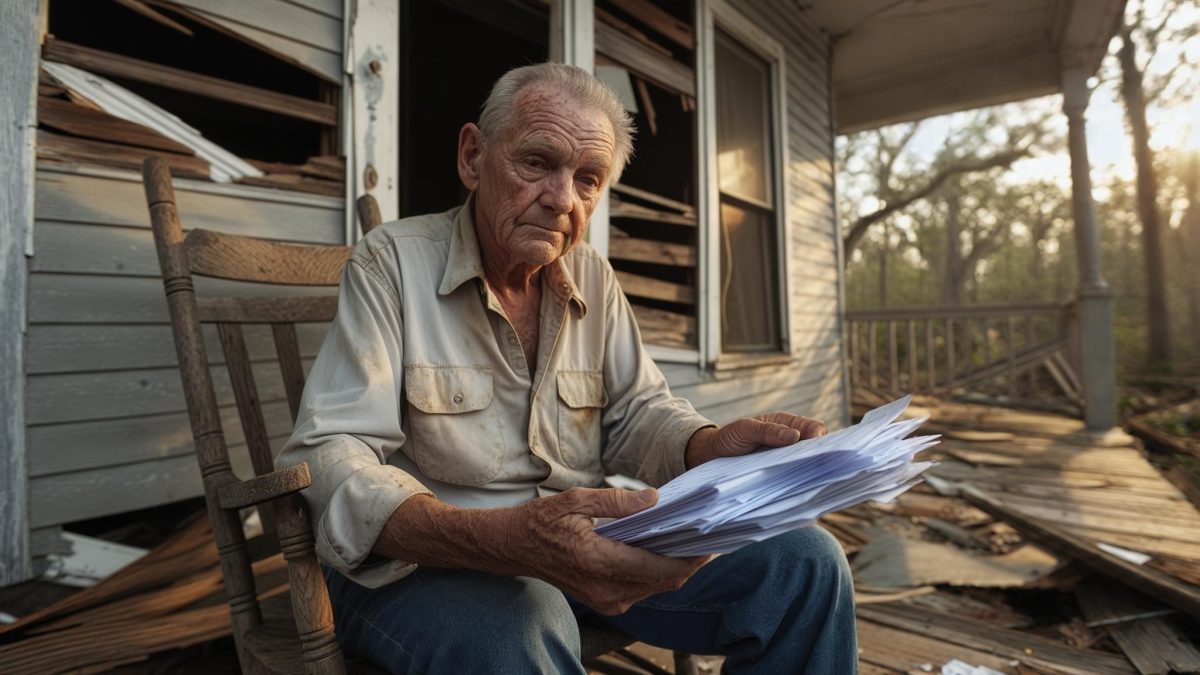

His mortgage was paid off — a genuine advantage — but his monthly fixed costs, including a car note, utilities, and what had been a $2,340 annual homeowner’s insurance premium, still left him recalibrating. Then, in May 2025, a severe storm caused hail damage to his roof and a section of his rear fence. He filed a claim. The repair payout came to $11,200. Two months later, in July 2025, he received a non-renewal notice from his insurer.

The insurer cited “claims history and elevated regional risk” in the non-renewal letter. Tommy called three other carriers over the following two weeks. Two declined to quote him at all. The third offered coverage at $6,100 per year — nearly three times what he had been paying.

The Scramble to Find an Alternative

Tommy’s first instinct was to handle it privately, the way he had handled most financial challenges in his life. He contacted a local independent insurance broker, who confirmed that the private market in Alabama had tightened sharply for homes with recent claims, particularly in Jefferson County, which had seen elevated storm-loss ratios through 2024 and 2025.

“The broker was honest with me,” Tommy said. “She told me straight up: ‘You’re going to have a hard time, and I don’t want to waste your time.’ That was actually helpful, even though it wasn’t what I wanted to hear.”

The broker pointed him toward the Alabama Department of Insurance, which oversees the state’s FAIR Plan — a program of last resort for homeowners who cannot obtain coverage through the private market. Alabama’s FAIR Plan is administered through the Alabama Insurance Underwriting Association and is not means-tested. Income does not determine eligibility.

Tommy had never heard of it. Neither, he told me, had either of his adult children when he called them for advice.

The Application Process — and What Actually Helped

Tommy submitted his FAIR Plan application in August 2025, roughly three weeks before his existing policy’s expiration date. The process was not seamless. His application required a property inspection, documentation of the prior claim’s resolution, and confirmation that no additional damage had gone unrepaired.

The inspection flagged a section of guttering that had been loosened in the same storm but not included in the original claim. Tommy paid $340 out of pocket to have it repaired before the re-inspection. The delay pushed his timeline uncomfortably close to his coverage lapse date.

Coverage was issued on September 12, 2025 — four days before his old policy would have lapsed. Tommy’s annual FAIR Plan premium came to $3,780. It was more than his original $2,340, and less than the $6,100 quote he had received from the one private carrier willing to take him. He described the moment he got the approval confirmation as one of the most quietly stressful experiences of the past year, finally releasing.

“Four days,” he said, shaking his head slowly. “I had four days of margin. If I hadn’t heard about the FAIR Plan when I did, I would have had a gap in coverage on a paid-off home. Do you know how bad that would have been if anything happened?”

A Small Win That Still Feels Fragile

By the time I spoke with Tommy in February 2026, he had been covered under the FAIR Plan for five months. He had also connected, through the Southside Community Resource Center, with a HUD-certified housing counselor who helped him build a revised monthly budget accounting for the lost overtime and the higher insurance premium.

According to the U.S. Department of Housing and Urban Development, HUD-approved housing counseling agencies provide free or low-cost financial guidance on a range of housing-related issues, including budgeting, mortgage assistance, and insurance challenges. The counseling itself cost Tommy nothing.

The revised budget reduced his discretionary spending by approximately $480 per month and redirected a portion of that toward a dedicated home-maintenance reserve — something the counselor had specifically recommended given the age of his property and its storm exposure history. Tommy described this as a meaningful structural change, even if it stung a little.

But he was candid about what still worried him. The FAIR Plan is not permanent security. Insurers can periodically re-enter or exit the Alabama market, and the plan’s premium structure can shift. More pressingly, his startup’s financial footing remained uncertain. He had heard informal talk of a possible acquisition that could eliminate his position entirely.

“I feel better than I did six months ago,” he told me near the end of our conversation, gathering his folder. “But I also know the ground can shift again. I’m 66. I’m not naive. I just don’t want to be caught flat-footed again the way I was.”

What struck me most as I drove back across Birmingham that afternoon was not the complexity of Tommy’s situation — it was how ordinary it was. He had done everything that a responsible homeowner is supposed to do. He owned his home. He carried insurance. He reported damage honestly. And still, through no particular failure of his own, he ended up in a gap that neither his income nor his diligence had insulated him from.

The programs that helped him — the FAIR Plan, HUD-certified counseling — were not secret. They were simply invisible to someone who had never been told to look for them. That invisibility, I kept thinking, was the real story.

Related: She Lost Her Home Insurance After One Claim — Then Her Spouse Retired and the Bills Kept Coming

Leave a Reply