The first time I heard Ruben Valdez’s name, I was standing in the fellowship hall of a small Presbyterian church on the north side of Spokane, Washington, on a wet Tuesday evening in January 2026. Pastor Elaine Torrez had pulled me aside after a community meeting I was attending for a separate story. She said she knew a man who’d spent his career crunching reservoir data and calculating risk for a living — and still couldn’t calculate his way out of a healthcare crisis. She thought I should talk to him.

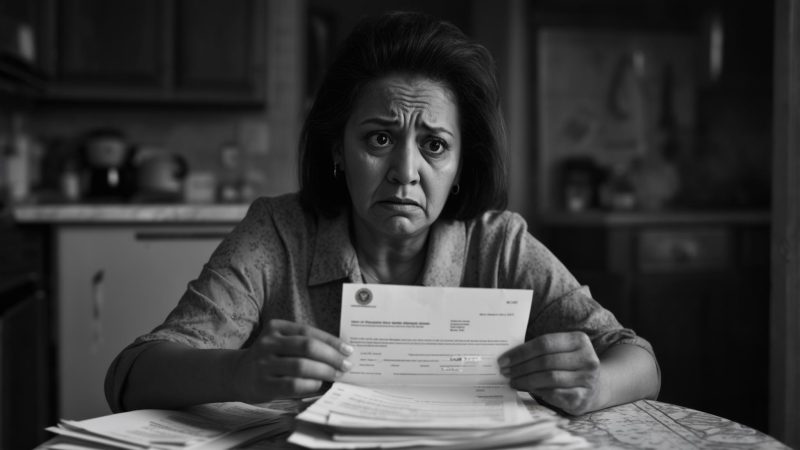

Ruben agreed to meet me at a diner near his apartment two days later. He arrived carrying a manila folder thick with explanation-of-benefits statements, insurance denial letters, and a printout of his monthly budget that he’d color-coded in three shades of red. He set it on the table between us like evidence.

A Career Built on Self-Sufficiency — and the Assumption It Would Last

Ruben Valdez has worked as an independent petroleum engineering consultant since 2011. Before that, he spent fourteen years on salary with a mid-sized energy company in Kennewick. When he went out on his own, he told me, it felt like the smartest financial move he’d ever made. His billable rate climbed to roughly $115 per hour, and in strong years he pulled in close to $95,000 after expenses.

The tradeoff, as any self-employed professional knows, was benefits. No employer-sponsored health plan, no employer contribution to a group policy. Ruben purchased an individual plan through the ACA marketplace for several years, paying around $620 per month in premiums. He told me he considered it a manageable cost of doing business.

In the spring of 2023, Ruben started noticing persistent pain in his lower back and left leg. By August, an MRI showed significant degenerative disc disease at L4-L5 and L5-S1, with nerve compression that his orthopedic surgeon described as “not optional to treat.” He had surgery in October 2023 — a microdiscectomy that cost $41,200 before his insurance applied. His out-of-pocket maximum that year was $8,700. He hit it in November.

The surgery helped, but not enough. Ruben needed ongoing physical therapy, pain management appointments, and a nerve stimulator evaluation. His capacity to work dropped sharply. Billable hours that once averaged 35 per week fell to 12 or 15. His 2024 income was approximately $38,000 — less than half of what it had been the year before.

When Disability Benefits Don’t Add Up

Ruben had paid into Social Security for over two decades. When his physician confirmed he could no longer perform sustained seated work without significant pain, he applied for Social Security Disability Insurance in February 2024. He was approved — faster than most, he acknowledged, largely because his documented medical record was thorough — and began receiving $2,190 per month in SSDI payments starting in May 2024, after the mandatory five-month waiting period.

That gap — between what SSDI paid and what his medical care actually cost — was the number Ruben kept returning to across our conversation. His monthly healthcare expenses averaged $3,840, including $620 in ACA premiums, $480 in physical therapy co-pays, $310 in medications, and ongoing specialist visits. The math wasn’t complicated. It was just brutal.

He was also, quietly, helping support his younger sister, Marisol, who was enrolled as a junior at Eastern Washington University. Ruben had been contributing $700 per month toward her tuition and living expenses. After his income collapsed, that number dropped to $300, a cut that required Marisol to take on additional student loan debt. Ruben described it to me as one of the outcomes that bothered him most.

The Medicaid Question — and Why It Wasn’t Simple

When Ruben first looked into Washington State’s Apple Health program — the state’s Medicaid expansion under the ACA — he assumed his situation would be straightforward. It wasn’t. The income eligibility threshold for adult Medicaid in Washington is set at 138% of the federal poverty level, which in 2024 translated to approximately $20,120 per year for a single adult. Ruben’s combined income — SSDI plus his reduced consulting earnings — exceeded that figure.

What Ruben didn’t initially know — and what a Washington Health Benefit Exchange navigator eventually walked him through — was that his unreimbursed medical expenses could, under specific circumstances, be deducted in what’s sometimes called a “medically needy” spend-down calculation. Washington does not have a traditional medically needy pathway for non-elderly adults, but the navigator helped him identify a different route: because his net income after medical costs fell below the poverty threshold in several months, he qualified for enhanced premium tax credits that substantially reduced his ACA marketplace costs.

By January 2025, Ruben had switched to a silver-tier marketplace plan with a subsidized premium of $148 per month — down from $620. That single change freed up $472 per month in his budget.

The Debt That Remained — and What Ruben Regrets

The premium reduction helped, but it didn’t erase the debt Ruben had already accumulated. By the time we spoke in January 2026, he owed approximately $19,400 across three medical providers — amounts that had gone to collections in two cases. He’d negotiated a payment plan on the largest balance, about $11,000 with the hospital system, at $250 per month with zero interest.

The regret in that statement was hard to miss. Ruben isn’t someone who makes excuses easily. He talked about his situation the way he might discuss a failed well projection: analytically, with a specific focus on what data he hadn’t accounted for. What he hadn’t accounted for, ultimately, was that the healthcare subsidy system contains eligibility pathways that aren’t prominently advertised and that most people don’t discover without help.

He told me he’s now eligible for Medicare in May 2026, when his 24-month SSDI waiting period ends. He expects his monthly healthcare costs to decrease further after that transition, though he acknowledged that Medicare Part B premiums, Part D drug coverage, and potential supplemental insurance costs mean the savings may be more modest than he initially hoped.

Picking Up What He Can

When I asked Ruben where things stood for his sister Marisol, his expression shifted. He’d managed to increase his monthly contribution back to $500 as his condition stabilized enough to allow more consulting hours — roughly 20 per week by late 2025. Marisol is on track to graduate in June 2026. He pulled out his phone and showed me a photo of her at a campus event. He didn’t say anything for a moment.

Ruben’s story doesn’t have a clean resolution. He still carries nearly $20,000 in medical debt. His earning capacity remains uncertain, tied to a physical condition that has good weeks and difficult ones. He’s 52, and the career trajectory he spent decades building has been permanently altered.

What changed, concretely, was that one phone call to a state insurance navigator in November 2024 restructured his monthly budget by $472. According to Healthcare.gov’s navigator program, certified navigators provide free, unbiased enrollment assistance — a resource that exists in every state but that many people, including someone as methodical as Ruben Valdez, don’t think to use until the financial damage is already accumulating.

Pastor Torrez told me after our meeting that she’d started keeping a short list of resources on a bulletin board near the church entrance — including the navigator program number. She’d started it because of Ruben. I thought about that on the drive back to my hotel: how many other people in that congregation, or in any congregation, were sitting on a coverage gap they didn’t know had a name.

Ruben walked me to my car in the parking lot of the diner. The temperature had dropped and there was a thin layer of snow on the asphalt. He said he was going back to finish updating a consulting report that was due the following morning. He still had the manila folder under his arm. He shook my hand and thanked me for listening. I thanked him for the spreadsheet.

Related: Claiming Social Security at 62 Cost Me $312 a Month — The Permanent Penalty Nobody Warned Me About

Leave a Reply