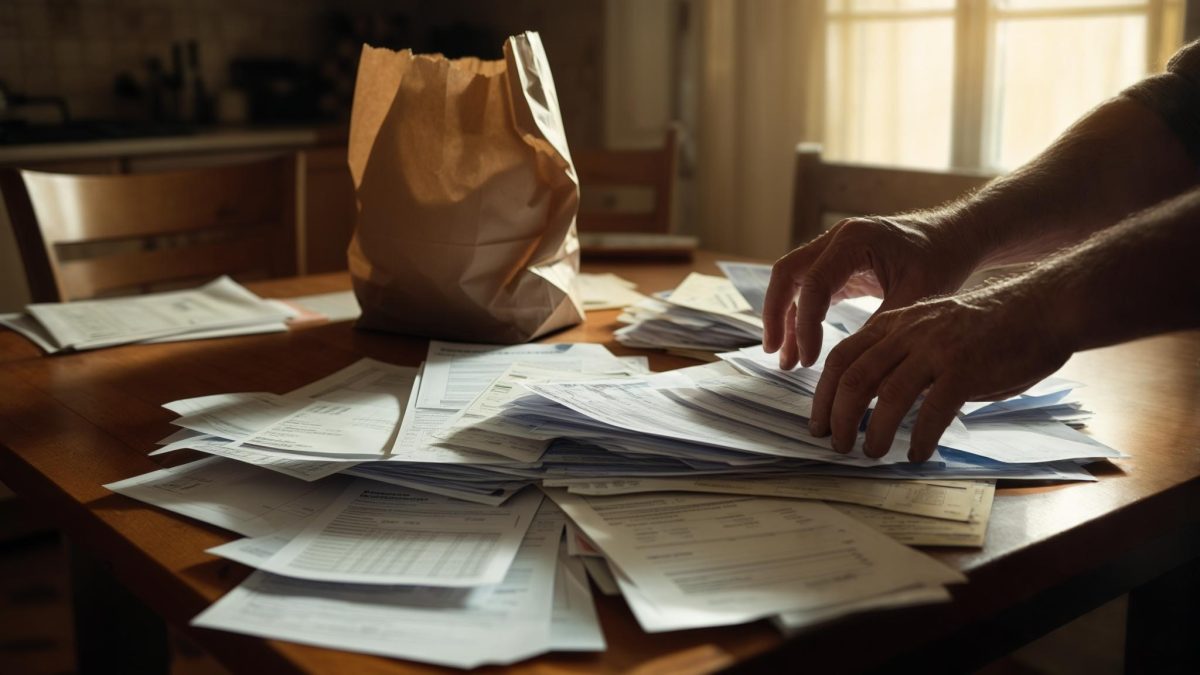

The manila folder on the table in front of Clint Santiago was thick enough to hold a small novel. Inside: mortgage statements, credit card bills that weren’t his, and a printed pay stub from a job he had held for nineteen years. He was at the St. Louis County Department of Social Services on a Tuesday morning in January, waiting to find out if he qualified for SNAP benefits. He was 65 years old. He made $72,000 a year. And he genuinely wasn’t sure he could afford groceries.

A social worker named Diane introduced me to Clint after I had spent the morning reporting on how Missouri residents were preparing for the federal SNAP changes rolling out in 2026. “You should talk to this man,” she said quietly. “He represents a side of this nobody talks about.” When I sat down with Clint Santiago across a small conference table, he spent the first five minutes apologizing for wasting my time.

When a Good Salary Stops Being Enough

Clint Santiago has been a legal secretary at a St. Louis law firm for nearly two decades. His gross salary is $72,000 a year — a number that, on paper, reads like comfort. He has a house in south St. Louis that he has owned since 2009. He drives a 2018 Honda Civic. His 88-year-old mother lives with him and relies on him for nearly everything.

Then, in October 2025, the floor dropped out. Clint’s wife of eleven years had passed away the previous spring. When the estate was settled and the accounts were closed, he discovered something that upended his financial life entirely: his wife had carried $48,000 in credit card debt across four accounts he had never known existed. Because they lived in Missouri — a state that treats certain marital debt jointly — collectors were coming for him.

His mortgage payment is $2,100 a month on a house that recently appraised at $285,000 — he owes $310,000. His mother’s prescription copays and medical appointments cost roughly $800 a month. His Honda Civic broke a timing belt in December 2025 and has sat in a mechanic’s lot ever since, waiting on a $3,200 repair he hasn’t been able to authorize. He commutes to work by bus.

After taxes, Clint’s take-home pay is approximately $4,400 a month. Once he accounts for the mortgage, minimum debt service payments on his late wife’s accounts, his mother’s medical costs, utilities, and the bus pass, he told me he has between $300 and $400 left for food — for two people.

What the SNAP Application Actually Showed Him

Clint applied for SNAP benefits through Missouri’s Family Support Division in December 2025. He described the process as more straightforward than he had expected — he submitted his application online, uploaded pay stubs, his mortgage statement, and documentation of his mother’s care costs, then waited. The denial came twelve days later.

The reason was unambiguous. According to SNAP eligibility rules codified under 7 CFR Part 273, gross income for most households must fall at or below 130% of the federal poverty level to qualify. For a two-person household in 2025–2026, that ceiling sits at approximately $2,137 per month. Clint earns $6,000 a month gross — nearly three times the threshold, before a single bill is paid.

The SNAP program does allow certain deductions — for dependent care, medical expenses for elderly household members, and excess shelter costs — but those deductions are only applied after a household clears the gross income threshold. Clint’s application never reached that stage. “I kept thinking, what if I’m missing something?” he told me. “What if there’s a deduction or a category I don’t know about? I even printed out the rules and read through them on my lunch break.”

There was no category that fit. His gross income was the ceiling, and the ceiling held.

The Bigger Picture: SNAP Is Changing Significantly in 2026

Even as Clint was navigating his own denial, the program he was trying to access was undergoing the most significant changes it has seen in years. Agriculture Secretary Brooke Rollins has been pushing sweeping reforms to SNAP, according to NPR’s reporting on the proposed rule changes. Those changes include expanded work requirements, reduced exemptions, and new restrictions on what recipients can purchase.

Starting February 1, 2026, according to Signal Cleveland’s coverage of the new work requirements, able-bodied adults without dependents between the ages of 18 and 54 must now document at least 20 hours per week of work or qualifying volunteer activity — or lose benefits after three months.

Texas went further still. Starting April 1, 2026, Texas banned the purchase of soda and candy using SNAP benefits, following a waiver from the USDA. Other states are expected to apply for similar exemptions in the months ahead.

I walked Clint through some of these changes as we talked. He listened with the focused attention of someone who had spent a month trying to understand a system from the outside. “So not only do people have to qualify,” he said, “but what they can buy is changing, and how much they have to work to keep it is changing. It’s a moving target for people who are already struggling to stand still.”

The Outcome: No Benefits, but a Different Kind of Clarity

Clint Santiago did not get SNAP benefits. He doesn’t qualify under current rules, and barring a dramatic change in income or household composition, he won’t. The social worker who introduced us had already connected him with a local food pantry network and a county-level emergency assistance fund for elderly caregiver households — resources that don’t require the same income verification that federal programs do.

The county emergency fund provided a one-time payment of $1,200, which Clint put toward one month of his mother’s medical copays. The food pantry has helped him stretch his grocery budget. His mortgage situation remains unresolved — he has submitted a loan modification request to his bank and has not yet received a response. The hidden credit card debt is now in negotiation with a debt resolution service. His car is still in the lot.

He hasn’t told his mother any of this. When I asked him about that, the pause before his answer was long enough that I didn’t rush it.

When I asked how he felt about the denial itself — whether it felt fair — he was more measured than I expected. “Relieved, honestly, that I know now,” he said. “I spent two months thinking maybe there was a net somewhere. Turns out there isn’t one for me. But knowing that is better than not knowing.”

What Clint’s Story Reveals About the Gaps in the System

Clint Santiago earns too much to qualify for federal food assistance but not enough — given his actual obligations — to feed himself and his elderly mother with any consistency. His situation illustrates a structural gap that policy researchers have noted for years: gross income thresholds don’t account for the layered financial burdens that can reduce a working person’s real purchasing power to almost nothing.

The Congressional Research Service’s primer on SNAP eligibility details the rules governing who qualifies — and those rules, however rationally constructed, weren’t designed for someone like Clint: a widower in his mid-sixties, newly responsible for a deceased spouse’s hidden debt, sole caregiver for an 88-year-old parent, and living on the edge of solvency while appearing, from the outside, to be doing fine.

- He earns above the SNAP gross income threshold by nearly $3,800 per month

- His real discretionary income after fixed obligations is under $400 per month

- He is the primary caregiver for an elderly parent with ongoing medical costs

- He carries marital debt he did not incur and did not know existed

- He has no functioning vehicle and no emergency savings remaining

None of those facts appear in the denial letter. The letter cited one line: income too high.

When I asked what he would say to someone else in his position — someone too proud or too embarrassed to walk through the door of a county assistance office — he didn’t hesitate.

As I drove back from St. Louis County that afternoon, I kept thinking about that manila folder — organized, tabbed, thorough. Clint had spent weeks assembling it for an application that had no field for what his life actually looked like. The system measured his income. It had no mechanism to measure what that income had to carry.

Clint Santiago is still taking the bus to work. He is still rationing meals some weeks. He is still making sure his mother doesn’t know. And he still apologized, at the end of our conversation, for taking up my time.

Related: Her Disability Benefits Paid 60 Cents on the Dollar — Then Her Insurer Dropped Her After One Claim

Related: A Nurse’s Salary, a Sick Parent, and $14,000 in Credit Card Debt: What One Spokane Woman Learned About Benefits She Was Owed

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply