Roughly 28 million Americans remain uninsured, according to estimates from the U.S. Census Bureau — but that figure doesn’t capture the specific kind of vulnerability facing the self-employed, where coverage gaps don’t always begin with poverty. Sometimes they begin with optimism.

I met Deshawn Parker on a Tuesday afternoon at a coffee shop on Woodward Avenue in Detroit. He had a laptop bag slung over one shoulder and a sketchbook tucked under his arm. He was 27, energetic, and kept glancing at his phone for client emails between sips of his coffee. He also had $14,000 in medical debt sitting in collections and a credit score he described, without flinching, as “destroyed.”

His story is not unique in its pain. It is specific in its details — and those details matter enormously for the millions of freelancers navigating America’s public health programs without a benefits coordinator to call.

The Leap and the Landing

Deshawn had been working a warehouse logistics job in the Detroit metro area for three years when he decided to go fully freelance in early 2023. He had been designing brand identities on evenings and weekends, pulling in an extra $800 to $1,200 a month on top of his salary. When a small agency offered him a three-month contract worth $12,000, he treated it as a signal.

“I had savings, I had clients, I had momentum,” he told me. “I thought, if I don’t do this now, I’m going to be in that warehouse until I’m 40 and wondering what happened.”

For a while, the gamble paid off. His first full year of self-employment brought in approximately $38,000 — not life-changing money, but enough to feel like proof. Then 2024 arrived with client cancellations, delayed invoices, and months where the work simply evaporated. He described the income swings as whiplash: $4,200 one month from a packaging project for a mid-size food brand, then $800 the next when a retail client paused their rebrand indefinitely.

What he didn’t do — and acknowledges plainly now — was enroll in health coverage after leaving the warehouse. His old employer had provided group insurance. Going freelance ended that. He knew he could shop the ACA marketplace, but unsubsidized premiums looked steep against months when his income barely cleared four figures. He kept telling himself he’d sort it out later.

A Night in the ER Changed the Math

In September 2024, Deshawn woke up at 2 a.m. with sharp pain in his lower right abdomen. He waited six hours — partly from denial, partly from the quiet financial calculation that millions of uninsured Americans run in the middle of the night — before a friend drove him to a Detroit hospital. He had appendicitis. The surgery was performed that morning.

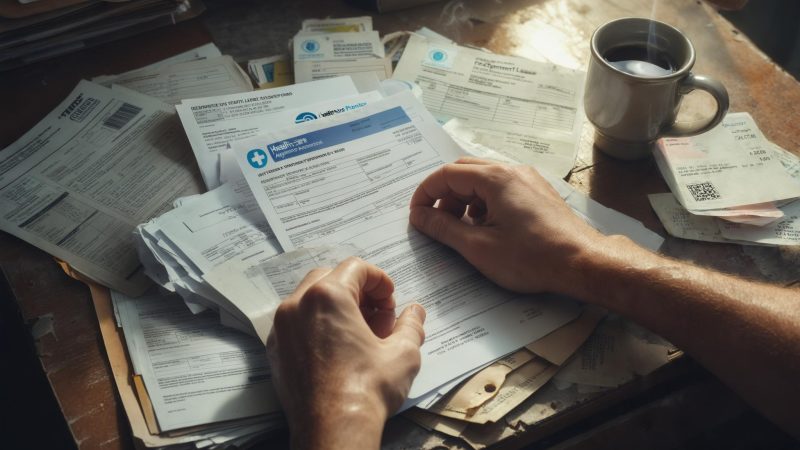

The bill arrived six weeks later: $14,312, itemizing the emergency room visit, the surgical procedure, anesthesia, a two-night inpatient stay, and follow-up medications. Deshawn had cleared around $1,100 that September. The number felt surreal on paper.

The debt transferred to a third-party collections agency in January 2025 — roughly four months after the surgery. At that point, negotiating directly with the hospital became significantly more complicated. His credit score, which he estimates sat in the mid-680s before the appendectomy, dropped sharply after the collections account appeared on his credit report.

What Deshawn didn’t know at the time was that nonprofit hospitals receiving federal funding are legally required to maintain financial assistance programs — sometimes called charity care — for patients who qualify based on income. Under IRS Section 501(r), these programs can reduce or eliminate bills for patients below certain thresholds. He found out about this option only after the debt had already left the hospital’s hands.

Navigating Medicaid as a Freelancer in Michigan

After the collections letter arrived, Deshawn started researching what he should have looked into two years earlier. He found Michigan’s Healthy Michigan Plan — the state’s Medicaid expansion program under the Affordable Care Act — which covers adults aged 19 to 64 who earn up to 138% of the federal poverty level. For a single adult in 2026, that ceiling is approximately $21,597 per year, or roughly $1,800 per month.

Deshawn’s situation was complicated by variable income. According to Healthcare.gov, Medicaid eligibility for self-employed applicants is typically based on projected annual income rather than any single month’s earnings — but how states implement and document that standard varies considerably. Michigan requires applicants to demonstrate income through records that salaried workers rarely need to compile.

“I thought it was going to be like applying for a job,” he said. “Fill out a form, they tell you yes or no. But they wanted income documentation, and my income is all over the place. I had invoices, bank statements, 1099s from two different clients. It took me three tries to get the documentation right.”

The process took nearly three months from first attempt to active coverage. During that window, Deshawn avoided seeing a doctor for a respiratory infection that dragged on for two weeks. “I knew I was sick but I kept thinking, I’ll wait until the card comes,” he told me. “Which is backwards. But that’s the mental space you’re in.”

Michigan’s Healthy Michigan Plan, administered by the Michigan Department of Health and Human Services, currently covers more than 800,000 adults statewide. For most enrollees, the plan carries a $0 monthly premium, with nominal cost-sharing requirements for those above 100% of the federal poverty level.

Where Things Stand Now — and What Didn’t Get Fixed

When I spoke with Deshawn in late March 2026, he had been enrolled in the Healthy Michigan Plan for just under a year. He’d used it twice — once for the respiratory infection he’d been deferring, and once for a dermatology referral. He called the coverage “genuinely life-changing” for his peace of mind, even though it arrived fourteen months too late for the appendectomy bill.

The $14,000 in medical debt is still sitting with the collections agency. He has made two payments of $200 each — the minimum the agency would accept as a show of good faith — but the principal has barely moved. His credit score, he told me, is somewhere in the low 590s.

There is some movement on medical debt nationally. In January 2025, the Consumer Financial Protection Bureau finalized a rule that would remove medical debt from consumer credit reports — a change that would have materially helped Deshawn’s score. That rule faced legal and regulatory challenges through 2025 and remains in an uncertain status as of early 2026, according to the CFPB. The agency has maintained that medical debt is a poor predictor of creditworthiness.

Deshawn keeps his Medicaid enrollment active by reporting significant income changes to the state — something the caseworker who processed his third application specifically instructed him to do. His income in February 2026 was $3,800, from a brand standards package for a Detroit-area restaurant group. January had brought in $950.

What Deshawn Says He’d Do Differently

Near the end of our conversation, I asked Deshawn what he’d tell another freelancer who was in his position two years ago — uninsured, income varying month to month, telling himself he’d handle the health coverage question eventually. He was quiet for a moment before answering.

“I’d tell them the health stuff is solvable,” he said. “Medicaid exists. You can get covered. But the part that happens when you don’t — the debt, the credit hit, the collections calls — that follows you. That part is much harder to undo.”

There is no clean resolution here. Deshawn Parker is talented, working, and now covered. He is also carrying a five-figure debt load that will take years to resolve, rebuilding a credit score from below 600, and managing an income structure the system was not designed to accommodate. His path to Medicaid coverage was slower and more costly than it needed to be — not because the program failed him, but because he didn’t know it was available until after the damage was already done.

He pulled the Medicaid card out of his wallet before we left. It was a little bent at one corner, like something actually used. That, at least, is something.

Related: A $14,000 Appendectomy Bill Went to Collections Before This Detroit Freelancer Could Even Pick Up the Phone

Related: A Detroit Freelancer’s $14K Medical Debt Went to Collections Before He Even Got the Bill

Leave a Reply