Arkansas’s Medicaid redetermination cycle — the annual process the state uses to confirm beneficiaries still qualify — was underway again this past March, with the Arkansas Department of Human Services issuing renewal notices to roughly 850,000 enrollees. For families like Aisha Hargrove’s, that cycle is never routine. It is a recurring source of dread.

I met Aisha through a mutual friend — a woman named Denise who had mentioned her at a neighborhood barbecue in Little Rock last October. Denise described Aisha in a way that stuck with me: “She does everything right and still can’t catch up.” I reached out the following week, and Aisha agreed to sit down with me at a diner near her apartment on a Tuesday morning before her shift.

Aisha Hargrove is 47, a retail store manager at a national chain in west Little Rock, and the primary caregiver for her 74-year-old mother, Loretta, who lives in a spare bedroom in Aisha’s two-bedroom apartment. She is not married. She has no retirement savings. And until eight months ago, her mother had no health coverage at all.

A Raise That Made Things Worse

The financial backdrop to Aisha’s story starts in early 2024, when she was promoted to store manager after six years as an assistant manager. Her salary increased from $38,400 to $46,500 annually — an $8,100 raise that felt, at the time, like a turning point.

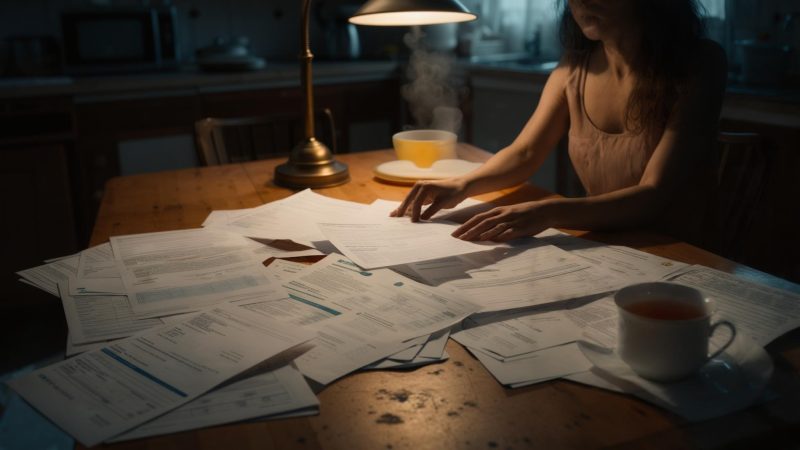

“I thought that raise was going to fix everything,” she told me, wrapping both hands around her coffee cup. “I got a bigger apartment so my mom could move in with me. I bought a used car because my old one was dying. I started paying for her medications out of pocket. And by month four, I had less left over at the end of the month than I did before the raise.”

Her mother, Loretta, has Type 2 diabetes and stage-two hypertension. Before moving in with Aisha, she had been living alone in Pine Bluff, skipping doses to stretch her medication supply. The three prescriptions she needed — metformin, lisinopril, and amlodipine — ran approximately $340 per month without insurance. Aisha absorbed that cost immediately.

This is what economists sometimes call lifestyle inflation: expenses that expand to meet — and then exceed — new income. For Aisha, it wasn’t frivolous spending. It was the cost of keeping her mother alive and off the street.

The First Two Denials

Aisha first applied for Arkansas Medicaid on her mother’s behalf in April 2024, approximately two weeks after Loretta moved in. The application was submitted online through the Arkansas My Benefits portal. Six weeks later, it was denied.

The denial letter cited “income above the eligibility threshold,” referring to Loretta’s Social Security benefit of $1,190 per month. At the time, Arkansas’s Medicaid income limit for a single adult age 65 and over was set at 100% of the Federal Poverty Level — approximately $1,255 per month in 2024. Loretta’s income appeared to fall just under that ceiling. Aisha was confused.

She appealed. The appeal was rejected in September 2024 on procedural grounds — a form had been submitted with her mother’s maiden name rather than her married name, creating a discrepancy in the identity verification system. Aisha found out about the mismatch three months after the fact, buried in a follow-up letter she almost didn’t open.

“I’ve managed a store for seven years,” she told me, a dry laugh escaping before she caught herself. “I deal with inventory systems and HR and scheduling for twenty-two employees. But that letter made me feel like I was failing a test I didn’t know I was taking.”

What Finally Changed

The turning point came in January 2025, when a caseworker at a local nonprofit — the Arkansas Connector Network, which provides free application assistance — reviewed Loretta’s file and identified two things Aisha had not known to pursue.

The approval arrived in a letter dated August 14, 2025. Aisha told me she read it twice before she believed it. She took a photo and sent it to her sister in Memphis before she even set it down.

The Relief Is Real, and So Is the Fear

Since Loretta’s Medicaid approval, Aisha has recaptured approximately $340 per month in medication costs. Her mother’s most recent A1C blood test — previously something Loretta skipped due to cost — came back with improved numbers, according to Aisha. The coverage has been, by any measure, a meaningful change.

But when I asked Aisha how she was doing — not her mother, but her — the answer was more complicated.

She is 47 years old with no retirement savings. Her current take-home pay, after taxes and a modest employee health insurance premium, is approximately $2,980 per month. Her rent is $1,050. Her car payment is $287. Utilities, groceries, and household expenses for two people consume most of what remains. She has roughly $1,400 in a checking account and no 401(k) contributions, active or historical.

“I know I’m behind,” she said matter-of-factly, the hopefulness she’d shown earlier shifting into something quieter. “I know what the numbers are supposed to look like. But when you’re choosing between your mother’s insulin and a retirement account, there is no choice. You do what you have to do.”

She paused, then added something that stayed with me long after I left the diner: “I’m proud that I kept us both going. I just hope that counts for something eventually.”

What Aisha’s Story Reveals About the System

Aisha’s experience is not an isolated failure. The application process for Medicaid — particularly for elderly enrollees who may qualify through multiple overlapping pathways — is structured in a way that penalizes people who don’t know what to ask for. The QMB program that ultimately helped Loretta is administered jointly by Medicare and state Medicaid agencies, but it requires a separate application and is not automatically triggered by a standard Medicaid denial.

Aisha lost sixteen months — and spent approximately $5,400 in out-of-pocket medication costs — during a period when her mother likely would have qualified for coverage, had the right application been filed correctly the first time.

When I asked Aisha what she would tell someone in her position — a caregiver trying to navigate a coverage application for an aging parent — she didn’t hesitate.

As I drove away from the diner that Tuesday morning, I kept thinking about the $5,400. Not because it’s a catastrophic sum in the national headlines sense, but because for Aisha Hargrove — a woman who managed a raise into a deficit, who took in her mother without hesitation, who fought a bureaucratic system for nearly two years — that money was the difference between having a financial cushion and having nothing. She still has nothing. But her mother has coverage. For now, that is what she is holding onto.

Related: She Lost $11,000 in Overtime and Her Rent Rose 30% — Then She Found Out Her Health Plan Was the Real Problem

Related: A Columbus Social Worker Was $4,200 Behind on Property Taxes — What He Found After He Finally Stopped Refusing Help

.pvv-faq-section details summary::-webkit-details-marker{display:none}.pvv-faq-section details summary::marker{display:none;content:””}.pvv-faq-section details[open] summary .pvv-faq-arrow{transform:rotate(90deg)}

Leave a Reply