Conventional wisdom says that a steady professional income is the best safety net you can have. Carmen Parker has a marketing manager title, a two-income household, and a mortgage in a quiet El Paso neighborhood — and she will tell you, with zero hesitation, that none of it was enough when her younger daughter ended up in the emergency room.

I first heard about Carmen at a block party last October, through a mutual neighbor who mentioned, almost in passing, that a couple down the street had been quietly drowning in medical debt for over a year. When I reached out, Carmen agreed to sit down with me at her kitchen table on a Saturday morning, her five-year-old playing in the next room. What unfolded over two hours was a story I’ve heard echoed across the country — the particular financial vertigo of earning just enough to be ineligible for help, but not nearly enough to absorb a catastrophic cost.

The Medical Emergency That Changed Everything

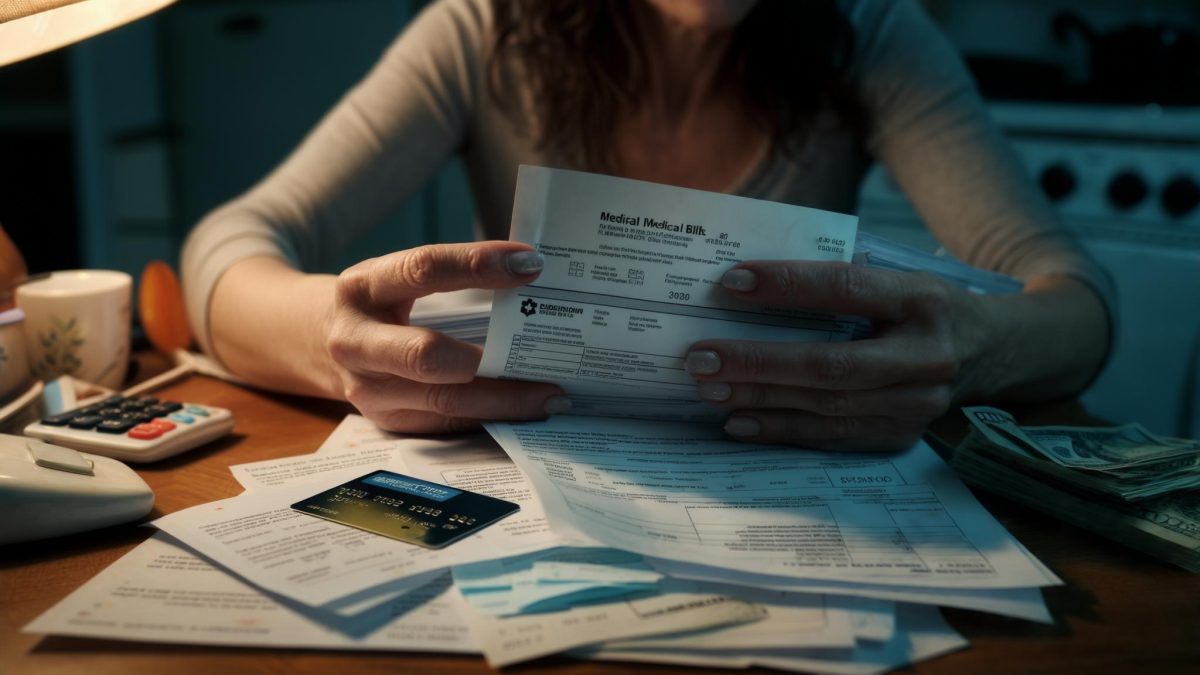

In February 2025, Carmen’s youngest daughter, Maya, was admitted to a hospital in El Paso with what initially presented as a severe asthma attack. It turned out to be a more complex respiratory issue requiring a two-night stay, imaging, and specialist consultations. The total bill arrived six weeks later: $14,200.

Carmen and her husband, Darnell, carry employer-sponsored health insurance through her startup job. But their plan came with a $6,000 family deductible — one they hadn’t come close to meeting before Maya’s hospitalization. After insurance processed the claim, the family owed $8,700 out of pocket.

“We didn’t have $8,700 in savings. Not liquid savings, anyway,” Carmen told me, her hands wrapped around a coffee mug. “We have retirement accounts, we have equity in this house. But cash? We were maybe two months out from having that kind of buffer. And then the bill arrived.”

She and Darnell split the bill across two credit cards. One carried a 22.99% APR. Within three months, with minimum payments and a family budget that was already strained, the combined balance had grown to just over $9,400.

The Family Obligation No One Talks About Openly

The medical debt didn’t land in a vacuum. Carmen is the financial anchor for extended family members — a role that carries real dollar figures most people outside immigrant and working-class communities never account for when calculating someone’s financial health.

Every month, Carmen sends approximately $400 to her mother in Juárez and contributes another $150 to $200 toward her younger brother’s rent in Phoenix, who was between jobs for most of 2025. That’s a floor of $550 per month leaving her household before groceries, childcare, or the mortgage.

As Carmen explained it, these transfers aren’t optional in any practical sense. They are the difference between her mother paying for blood pressure medication and skipping it. They are what kept her brother from eviction. The $550 is not discretionary spending — it functions more like a parallel household expense that no budgeting app she’s tried has ever categorized correctly.

When the medical debt arrived, Carmen didn’t consider stopping the transfers. She considered stopping almost everything else first.

Exploring Medicaid — and Running Into the Coverage Wall

In the weeks after Maya’s hospitalization, Carmen began researching whether any of her family members might qualify for Medicaid or CHIP coverage — particularly Maya and her eleven-year-old son, Marcus. She spent several evenings on the HealthCare.gov eligibility screener and the Texas Health and Human Services portal.

Texas has not expanded Medicaid under the Affordable Care Act, which means the income threshold for adults remains extremely low. For children, CHIP eligibility in Texas extends to families earning up to 201% of the federal poverty level. Carmen’s household income — approximately $98,000 combined, with Darnell’s part-time work — put them well above that threshold.

“I knew we made too much. I wasn’t naive about that,” Carmen said. “But I thought maybe there was something I was missing. Some program. Some exception. There wasn’t.” She paused. “I spent probably twelve hours total on those websites. Twelve hours to confirm what I already suspected.”

She did find one partial path forward: the hospital’s own charity care program. After submitting financial documentation — two years of tax returns, pay stubs, a list of monthly obligations including the family remittances — the hospital agreed to reduce the remaining balance by $1,800. It brought their total owed down to roughly $6,900 across the two credit cards.

The Slow, Unglamorous Climb Back

When I spoke with Carmen in early March 2026, she and Darnell had paid down approximately $3,100 of the original credit card debt over twelve months. The remaining balance sat at $6,200 — not because they weren’t trying, but because the interest rate on the higher-APR card had cost them an estimated $1,400 in charges during that period alone.

She’d requested a balance transfer to a lower-rate card in late 2025 and moved $4,000 of the debt to a card with a 0% promotional period. That window closes in August 2026, which Carmen describes as a hard deadline she thinks about daily.

She’d also made one difficult call: reducing the monthly transfers to her brother in Phoenix to $75 while he found steadier work. Her mother’s $400 remained unchanged. “My mom’s medication doesn’t negotiate,” Carmen said flatly. “Marcus’s extracurricular activities negotiate. My brother’s monthly contribution negotiated. My mom’s pills do not.”

What Carmen Wishes She Had Known Earlier

By the end of our conversation, Carmen had shifted into the kind of reflective mode that comes from having processed something long enough to see its edges clearly. She’s analytical by nature — she’d brought a folder of printed documents to our interview, including the hospital’s charity care application and both credit card statements — and she’d spent considerable time mapping out what she would do differently.

The charity care application was at the top of her list. She hadn’t known it existed until a social worker at the hospital mentioned it during discharge — over a week after Maya had been admitted. She wonders how many families never hear about it at all.

- Ask about hospital financial assistance programs before or immediately after discharge — not weeks later when the bill arrives

- Request an itemized bill and review it for errors before making any payment arrangements

- Contact your state’s insurance commissioner if a claim denial seems inconsistent with your plan documents

- Document family financial obligations — including informal transfers — when applying for any income-based assistance program

She also expressed something close to frustration with the binary nature of means-tested programs. According to Medicaid.gov’s eligibility guidelines, program criteria are set at the state level and can vary dramatically — which meant Carmen’s experience in Texas would have been entirely different had her family lived across the border in New Mexico, where Medicaid expansion covers adults up to 138% of the federal poverty level.

“I’m not asking for a handout,” she told me near the end of our conversation, and I believed her entirely. “I’m asking for a system that acknowledges that earning $98,000 and having $550 a month in family obligations and an $8,700 medical bill are not mutually exclusive realities.”

A Story Without a Clean Ending

Carmen’s situation, as of our conversation, is not resolved. The $6,200 balance is real, the August deadline is approaching, and Darnell has picked up a few additional hours that may or may not be permanent. She’s cautiously optimistic about the next six months. She is also, as she put it, “constitutionally incapable of not worrying.”

What struck me most was not the debt itself — though the numbers are significant — but the compound weight of it. The way a single emergency had exposed every other tension point in the family’s finances: the remittances, the thin savings buffer, the insurance plan that worked fine until it suddenly didn’t. The sense that she had done everything right and still found herself in a place that felt distinctly wrong.

Before I left, Maya ran into the kitchen and asked her mother something about a cartoon. Carmen answered without missing a beat, then looked back at me and smiled — the particular smile of someone who has learned to hold two realities at once. The family is okay. The family is also in debt. Both things are true, and neither cancels the other out.

That is, I think, the story that most income brackets never bother to tell.

Related: One Medical Emergency Added $34,000 to This Richmond Dad’s Credit Cards — Now He’s Rethinking Everything

Related: I Met Sheila at a Pharmacy Counter. Her Story About Medical Debt and a Tax Credit She Almost Missed

Leave a Reply